.png)

Independent semiconductor channel intelligence from Edgewater Research, TrendForce, IDC, and supplier disclosures from leading manufacturers including ASML, Samsung, and Micron collectively confirm that the global electronics supply chain has transitioned out of post-correction inventory normalization and is entering a demand-driven tightening cycle.

Recent market checks indicate order momentum accelerated during late 2025, with book-to-bill ratios across multiple semiconductor categories exceeding 1.1x — a leading indicator historically associated with multi-quarter supply expansion phases. These shifts coincide with expanding backlog visibility across semiconductor, IP&E, and power electronics supply chains.

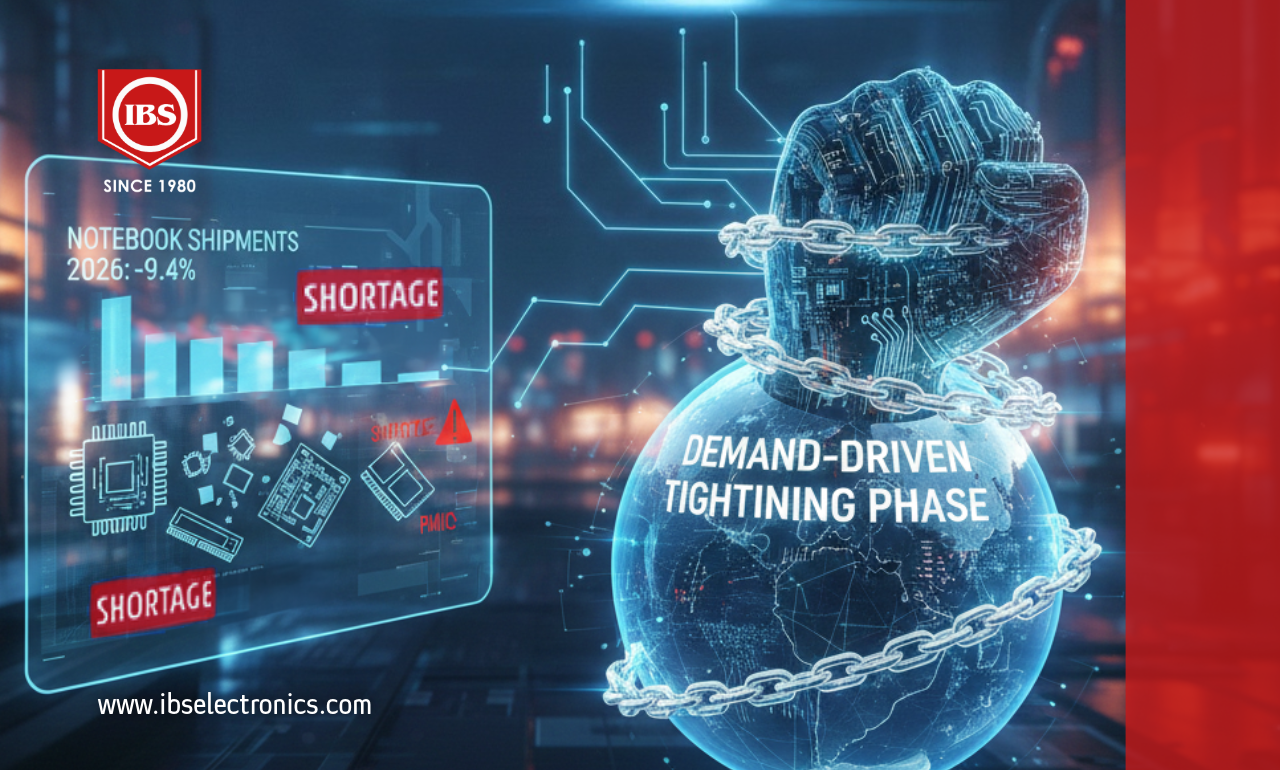

Simultaneously, industry shipment forecasts illustrate emerging supply constraints. According to TrendForce analysis cited in the Electronics Supply Chain Weekly Digest, global notebook shipments are projected to decline 9.4% year-over-year in 2026 due to shortages of CPUs, memory, PCBs, and power management components. These indicators reflect early structural tightening rather than cyclical fluctuation.

Memory Allocation: The Primary Supply Constraint Reshaping Electronics Manufacturing

Memory Allocation: The Primary Supply Constraint Reshaping Electronics Manufacturing

Memory supply is currently the most measurable bottleneck across global electronics manufacturing. Channel intelligence from confirms Taiwanese memory suppliers are quoting DDR4 pricing near $10 per gigabyte — materially exceeding late-2025 projections and signaling accelerated demand imbalance. More critically, supplier feedback indicates DDR4 production capacity is effectively sold out for 2026 and is now being allocated primarily to strategic customers and long-term supply agreement participants.

Allocation restrictions are already producing downstream risk. Automotive Tier-1 suppliers have reported receiving only 30-40% allocation commitments from certain memory manufacturers, with potential production shortages exceeding 50% for memory-dependent vehicle architectures under worst-case allocation scenarios.

Major memory manufacturers themselves confirm sustained constraint risk. Samsung Electronics and SK Hynix have publicly indicated that limited cleanroom expansion capacity and unprecedented growth in high-bandwidth memory demand could extend supply shortages through 2027.

Lead Time Expansion Confirms Broader Semiconductor Supply Tightening

Lead time expansion across analog, discrete, and power semiconductor markets is occurring simultaneously — historically a reliable early indicator of extended tightening cycles. Supplier channel checks indicate:

- Analog component lead times have extended from approximately 10–12 weeks to 18–20 weeks on average

- Power management ICs and DSP products are experiencing increasing supply constraints driven by substrate availability

- Low-end FET devices are now routinely quoting lead times approaching 52 weeks, driven by packaging and substitution supply limitations

- PCB supply is tightening due to increased demand from AI server manufacturing

These shifts are compounded by increased utilization of mature 200mm wafer fabrication processes. Industry channel checks suggest utilization levels, previously running near 60-70%, are expected to rise sharply in 2026 as automotive, defense, and RF semiconductor demand expands simultaneously.

Artificial Intelligence Infrastructure Is Restructuring Global Semiconductor Demand

AI infrastructure investment is rapidly reshaping semiconductor capacity allocation worldwide.

ASML reported record bookings in 2025 with $15.8 billion in quarterly orders, including $8.9 billion tied specifically to extreme ultraviolet lithography equipment used in advanced logic and memory fabrication. ASML has forecast 2026 revenue between $40.8 billion and $46.8 billion, reflecting sustained capital expansion across advanced semiconductor manufacturing.

Simultaneously, TrendForce projects global shipments of AI compute ASICs to triple by 2027 as hyperscale cloud providers, including Google, Microsoft, Meta, and AWS, continue vertically integrating custom AI silicon into their infrastructure platforms. These capital investments are diverting wafer capacity toward advanced computing programs and reducing manufacturing flexibility across mature semiconductor nodes supporting automotive, industrial, aerospace, and renewable energy electronics.

Commodity Inflation Is Amplifying Component Cost Pressures

Raw material inflation is now materially impacting electronics component production costs.

Supply chain checks indicate shortages in silver supply affecting high-performance battery manufacturing and electric vehicle production, with reports of delivery challenges from the London commodities exchange impacting multiple industries reliant on advanced energy storage technologies.

Simultaneously, passive component manufacturers are implementing pricing increases tied directly to rising metal input costs and AI-driven demand expansion. Yageo, one of the world’s largest passive component manufacturers, recently announced resistor price increases ranging from 15–20% linked to metal raw material inflation and expanding electronics demand.

These commodity cost increases directly impact connector plating, termination systems, semiconductor packaging, and PCB manufacturing across multiple industries.

Sector Demand Convergence Is Increasing Allocation Competition

The tightening supply environment is further amplified by simultaneous growth across traditionally independent electronics sectors.

Automotive Electronics

Automotive semiconductor content continues expanding due to electrification, ADAS deployment, and digital cockpit architectures. Memory shortages are increasingly viewed as a primary constraint to automotive production growth, particularly as ADAS systems transition toward DDR5-dependent architectures.

Industrial Automation and Energy Infrastructure

Industrial equipment demand has begun inflecting positively after multiple quarters of contraction. Channel checks indicate strengthening demand across semiconductor equipment, industrial automation, and energy infrastructure programs entering 2026.

Aerospace and Defense

Defense electronics demand is accelerating globally, particularly within drone technologies and communications infrastructure. Many of these programs rely heavily on mature-node semiconductor processes, intensifying competition for 200mm wafer supply capacity.

Renewable Energy and BESS Infrastructure

Battery energy storage expansion, grid modernization, and power conversion technologies continue driving sustained demand for power semiconductors, passive components, and interconnect technologies. Commodity material inflation and wide-bandgap semiconductor adoption are reinforcing supply constraint risks across this sector.

Pricing Discipline Is Re-Emerging Across Semiconductor Suppliers

After several years of pricing volatility driven by excess inventory, semiconductor manufacturers are re-establishing pricing discipline. Supplier-specific feedback indicates Analog Devices is actively pursuing 10–15% price increases across select component portfolios, citing higher input costs, substrate inflation, and tightening supply conditions.

Texas Instruments has also been observed implementing selective price increases in some cases months after annual customer pricing negotiations, reflecting increasing supplier leverage during tightening market conditions.

Procurement Behavior Is Transitioning Toward Supply Assurance

One of the most significant structural shifts across electronics manufacturing is the transition from cost-optimization procurement to supply-assurance procurement. Industry channel checks confirm manufacturers are:

- Increasing safety stock targets

- Expanding long-term supply agreements

- Accelerating purchase commitments

- Increasing dual-source qualification programs

Several EMS providers have reported ordering up to one year of component supply within single quarters to protect against allocation risk — a behavior pattern historically associated with early tightening cycle acceleration.

Market Forecast: Evidence Supports a Multi-Year Constraint Expansion

Current supply chain indicators strongly suggest the electronics industry is entering an extended tightening cycle expected to continue through at least 2027.

Key measurable indicators include:

- Memory capacity constraints forecast to persist through 2027

- Advanced semiconductor packaging and substrate supply expected to remain limited

- AI infrastructure investment projected to absorb incremental semiconductor capacity growth

- Mature-node semiconductor utilization rates expected to increase significantly throughout 2026

Strategic Implications for OEM, EMS, MRO, and Energy Infrastructure Operators

Market intelligence suggests manufacturers and infrastructure operators should consider immediate strategic adjustments:

- Expand production forecasting beyond quarterly planning cycles

- Secure allocation commitments through long-term supplier alignment

- Diversify sourcing and qualification programs

- Integrate lifecycle supply planning into engineering design phases

- Strengthen distributor partnerships to enhance real-time supply intelligence

Market Conclusion

Data from supplier disclosures, semiconductor capital investment trends, channel intelligence, and commodity market signals collectively confirm that the global electronics supply chain is entering a structurally tightening demand cycle.

The next 24–36 months will be defined less by price negotiation and more by supply continuity, allocation access, and forecasting discipline. Organizations that build proactive procurement strategies, strengthen supplier collaboration, and expand supply visibility will be best positioned to manage cost volatility and production risk.

The indicators are not speculative — they are measurable, validated across multiple industry intelligence sources, and accelerating.

As these market dynamics continue to evolve, IBS Electronics provides customers with global visibility into component availability, allocation risk, and supplier behavior across semiconductor, IP&E, and electromechanical markets. Leveraging decades of multi-regional sourcing intelligence, IBS supply chain specialists actively monitor shortage indicators, lead-time movements, and lifecycle risk signals to help customers anticipate disruptions before they impact production or maintenance operations.

Through proactive supply planning, alternative sourcing qualification, and real-time market intelligence, IBS Electronics Group supports OEM, EMS, MRO, and renewable energy infrastructure customers in navigating tightening supply environments while maintaining operational continuity. As supply cycles become increasingly complex and demand patterns accelerate, IBS remains committed to helping customers stay ahead of shortages, protect production schedules, and stabilize procurement strategies through data-driven supply chain expertise.

Are your components secure through 2027?

Stay ahead of risk. Plan for a multi-year cycle.

Why We Are One

For over 40 years, IBS Electronics Group has provided a broad range of integrated supply chain and electronicsmanufacturing solutions tailored specific to our customer's operations. As your one source for the industry’s top brands all in one place, our engineers specialize in reducing supply chain complexity and are here to provide you with dedicated support from prototype to production.

.png?resizemode=force&maxsidesize=96)