AI Demand Pushes WSTS 2025 Chip Forecast Up to $772B

Published: 12.11.2025

Logic and memory drive a sharper rebound as AI reshapes global demand

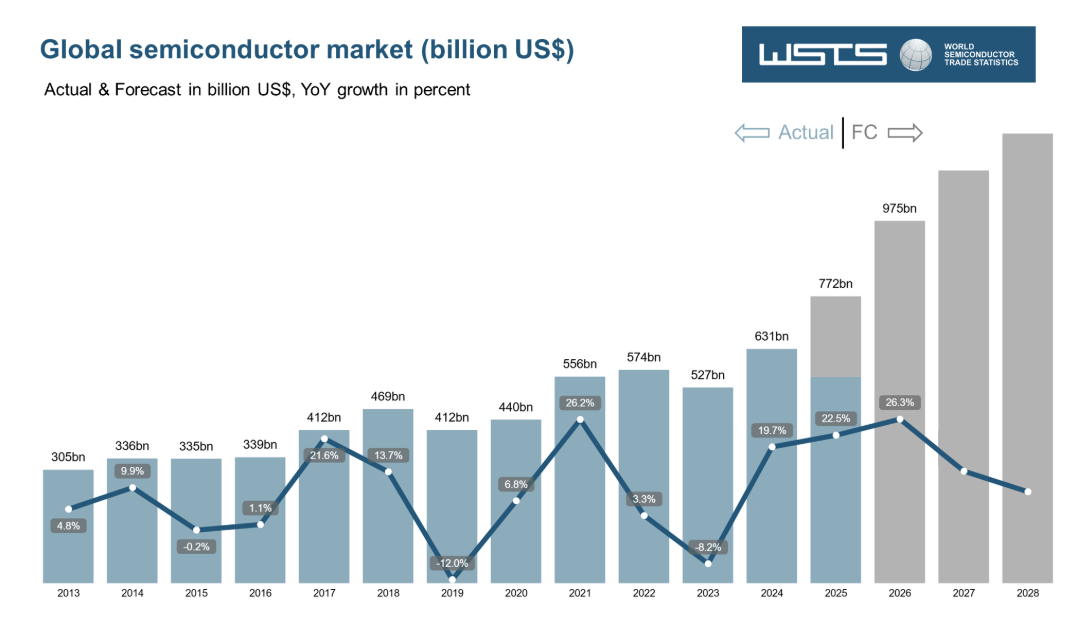

The semiconductor industry just received one of its strongest outlook upgrades in recent years. The World Semiconductor Trade Statistics organization now expects the global chip market to reach USD 772 billion in 2025, up nearly 22% year-on-year and a substantial jump from WSTS’ earlier forecast of USD 700.9 billion released in Spring 2025.

The revision follows a stronger-than-anticipated third quarter, adding almost USD 45 billion to the 2025 outlook and lifting expected growth by more than seven percentage points, reinforcing what the market has been signaling all year: the 2023 downturn is firmly behind us and demand is accelerating faster than most analysts projected.

This upgraded 2025 semiconductor market forecast sends a clear signal that the next design and sourcing cycle will be shaped by AI, logic, and memory at a scale the industry has not seen before.

Many industry watchers now believe this trajectory could push the global semiconductor market close to USD 1 trillion as early as 2026. WSTS itself forecasts about USD 975 billion in 2026, underscoring how quickly AI, data centers, and electrified systems are reshaping global semiconductor demand.

Why the Forecast Jumped: AI, Logic, and Memory

WSTS stated that the upgrade comes from a strong rebound in logic and memory that power AI servers, cloud infrastructure, and high-performance systems. As demand for accelerators, GPUs, CPUs, and high-bandwidth memory climbs, these categories are driving the market higher.

For 2025, WSTS expects logic revenue to grow by around 37% year-on-year, while memory revenue rises by nearly 28%. AI infrastructure is driving robust demand for high-bandwidth memory, advanced logic nodes, and the power components that support them.

Other segments, such as analog, sensors, and optoelectronics, are set for moderate growth. Discrete components appear roughly flat due to softer demand in certain automotive segments. In practical terms, this means market growth is becoming increasingly concentrated around AI, data centers, and compute-intensive systems, rather than being evenly distributed across all device categories.

Where the Growth Is Coming From

The 2025 outlook also shows a shift in regional momentum:

- Americas are projected to grow nearly 30%, supported by strong investments in AI compute, cloud infrastructure, and leading chip design houses.

- Asia-Pacific is expected to grow roughly 25%, reflecting its dominant role in manufacturing, packaging, and test operations.

- Europe will see slower mid-single-digit growth, driven by industrial, automotive, and defense digitization.

- Japan may contract slightly, though it remains influential in materials, equipment, and specialty semiconductors.

A Market Racing Toward the Trillion-Dollar Era

If WSTS’ numbers hold, the industry is entering one of the fastest expansions in its history. The global semiconductor market is expected to grow from roughly USD 630 billion in 2024 to USD 772 billion in 2025, then push toward USD 975 billion in 2026.

Between 2024 and 2026, that adds more than USD 340 billion in additional annual revenue a kind of growth curve that has traditionally taken a decade or more to materialize. This wave of expansion signals a fundamental shift in how the industry operates. AI has become the anchor of global semiconductor demand, influencing everything from server design and memory roadmaps to how power, passives, and interconnect solutions are chosen.

Unlike past cycles, this one is pulling both mature nodes and advanced nodes forward at the same time. AI PCs, high-speed networking, EV platforms, industrial automation, and high-capacity storage are all leaning on different parts of the technology stack, creating shared momentum across 28 nm, 14 nm, 7 nm, and leading-edge geometries.

At the same time, investment cycles are speeding up. Foundries, OSAT providers, and materials suppliers are planning for 2026 through 2030, not just the coming year. They are building capacity and capability for a world where AI, data centers, and electrified systems keep climbing, while governments use subsidies, export rules, and industrial policies to influence where that capacity ends up. Markets like Vietnam, India, and parts of Southeast Asia are stepping more actively into the global semiconductor map as supply chains diversify.