EV Traction Inverter Installations Surge 19% in Q2 2025

Published: 9.16.2025

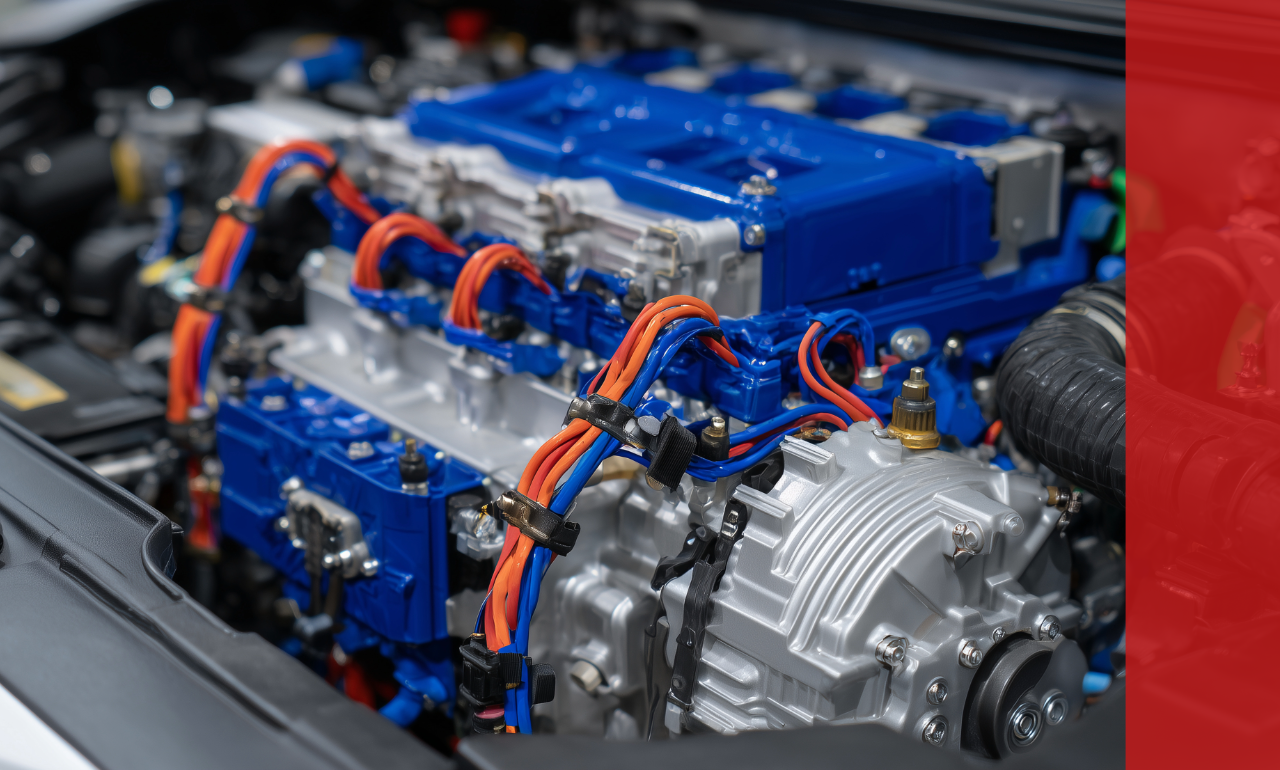

Global demand for electric vehicles is reshaping the power semiconductor landscape, with worldwide EV traction inverter installations reaching 7.66 million units in Q2 2025 with a 19% year-on-year increase, according to TrendForce.

Battery electric vehic led the market with more than half of inverter installations, while hybrids, plug-in hybrids and range-extended EVs also showed steady growth. REEV adoption, in particular, is driving broader use of advanced power technologies.

A key trend is the growing penetration of silicon carbide (SiC) inverters, now accounting for 17% of all units installed. While BEVs remain the largest driver of SiC adoption, REEVs and PHEVs are quickly integrating the technology—together making up nearly one-fifth of SiC inverter demand.

On the supply side, Tier-1 suppliers continue to consolidate share: BYD leads with 17%, followed by Denso at 14%, while Huawei and Inovance are gaining traction as BEV and REEV demand grows.

Impact on the Supply Chain

The rise of traction inverter demand and the shift toward SiC is creating ripple effects across the electronic components supply chain:

- Rising SiC demand: Suppliers must expand wafer capacity and improve yields amid intensifying global and Chinese competition.

- Supporting components: Gate drivers, passive components, and advanced thermal management are increasingly critical for reliable performance.

- Cross-sector impact: Advances in EV inverters are expected to accelerate SiC adoption in renewable energy systems, including solar, wind, and battery storage, where efficiency and thermal management are key.

As automakers expand EV offerings, traction inverters are becoming a strategic battleground for cost competitiveness and supply chain resilience. For semiconductor and electronic component suppliers this goes beyond automotive and signals broader opportunities in power and renewable energy applications worldwide.