IBS Analysis: TrendForce Upgrades 1Q26 Memory Price Forecast as Prices Surge

Published: 2.18.2026

Key Takeaways

- TrendForce now projects conventional DRAM contract pricing up 90–95% QoQ and NAND flash up 55–60% QoQ in 1Q26, with enterprise SSDs up 53–58% QoQ, a major escalation versus its January view.

- The story is no longer just demand but an allocation discipline. TrendForce says suppliers are steering advanced-node capacity toward server DRAM and HBM-adjacent demand, tightening availability for PC, mobile, and conventional categories.

- Procurement is shifting from price shopping to coverage strategy: LTAs, selective buffer stock on critical SKUs, early alternate qualification, and stricter PCN/EOL monitoring, especially where flash transitions can force re-validation.

A memory rebound is familiar territory. What is unfolding in early 2026 looks different.

In its latest market update, TrendForce raised its 1Q26 contract-price outlook for both DRAM and NAND flash, warning that the industry has entered a phase where allocation discipline and AI server demand are reshaping pricing power across the supply chain. The firm now projects conventional DRAM +90–95% QoQ, NAND +55–60% QoQ, and enterprise SSD +53–58% QoQ in 1Q26, a record-level increases across categories for the quarter.

January vs February: What Changed?

TrendForce’s January forecast already pointed to a sharp recovery. The February revision reflects tighter-than-expected supply conditions and more aggressive procurement behavior, particularly from cloud service providers (CSPs) and server OEMs supporting AI infrastructure buildouts.

| Segment (1Q26 contract pricing) | TrendForce January View | TrendForce February Update |

|---|---|---|

| Conventional DRAM | +55–60% QoQ | +90–95% QoQ |

| NAND flash | +33–38% QoQ | +55–60% QoQ |

| Enterprise SSD | (rising; enterprise becoming largest segment) | +53–58% QoQ |

IBS chart recreated from TrendForce forecast ranges (Jan 5 vs Feb 2, 2026).

IDC has also warned the current memory shortage could persist well into 2027, suggesting non-hyperscale buyers should plan for extended pricing and allocation pressure beyond 2026.

From Recovery to Repricing

Memory markets normally move through oversupply, correction, inventory digestion, and recovery. What TrendForce is describing now signals the market has moved beyond recovery into repricing, because supply is being steered.

TrendForce noted that suppliers are reallocating advanced-node capacity and new output toward server DRAM and HBM-related demand to meet AI-server pull, tightening the pool available for PC/mobile/embedded segments.

That framing aligns with supplier commentary as Micron has indicated AI-driven memory demand continues to outstrip supply into 2026, reinforcing that this isn’t a short “restock” event. It’s a capacity-and-allocation story.

AI Infrastructure as a Structural Pull

AI clusters depend on high-capacity server DRAM and fast enterprise storage, and deployments are often tied to hyperscaler capex schedules. Once that rollout is committed, memory becomes a must-ship input rather than a flexible purchase.

TrendForce highlighted strong enterprise SSD order momentum, particularly from North American CSPs, while warning that broader buyers face supply gaps.

For everyone outside hyperscale supply chains, the near-term risk becomes less “how high will prices go?” and more whether supply remains available on production timelines.

Implications for OEM/EMS + industrial/medical/aerospace programs

- Higher likelihood of allocation constraints on mainstream DRAM and NAND SKUs

- Increased importance of qualification timelines (industrial controllers, medical systems, avionics/mission systems, long-life platforms)

- Greater exposure to PCNs/EOLs becoming schedule risks

- A procurement advantage for teams with secured capacity and qualified alternates

DRAM Tightness Is No Longer Isolated

TrendForce’s February upgrade indicates tightening is no longer confined to the server segment; it also signals stress in PC and mobile, noting PC DRAM pricing could at least double QoQ in 1Q26.

That “spillover” matters to embedded buyers because many long-life designs source from the same manufacturing ecosystem, and supplier allocation decisions can propagate quickly into conventional categories.

S&P Global Market Intelligence (Visible Alpha) has also noted that HBM’s structurally higher pricing can incentivize suppliers to prioritize AI-linked HBM output, tightening supply for traditional DRAM categories and amplifying pricing pressure in 2026.

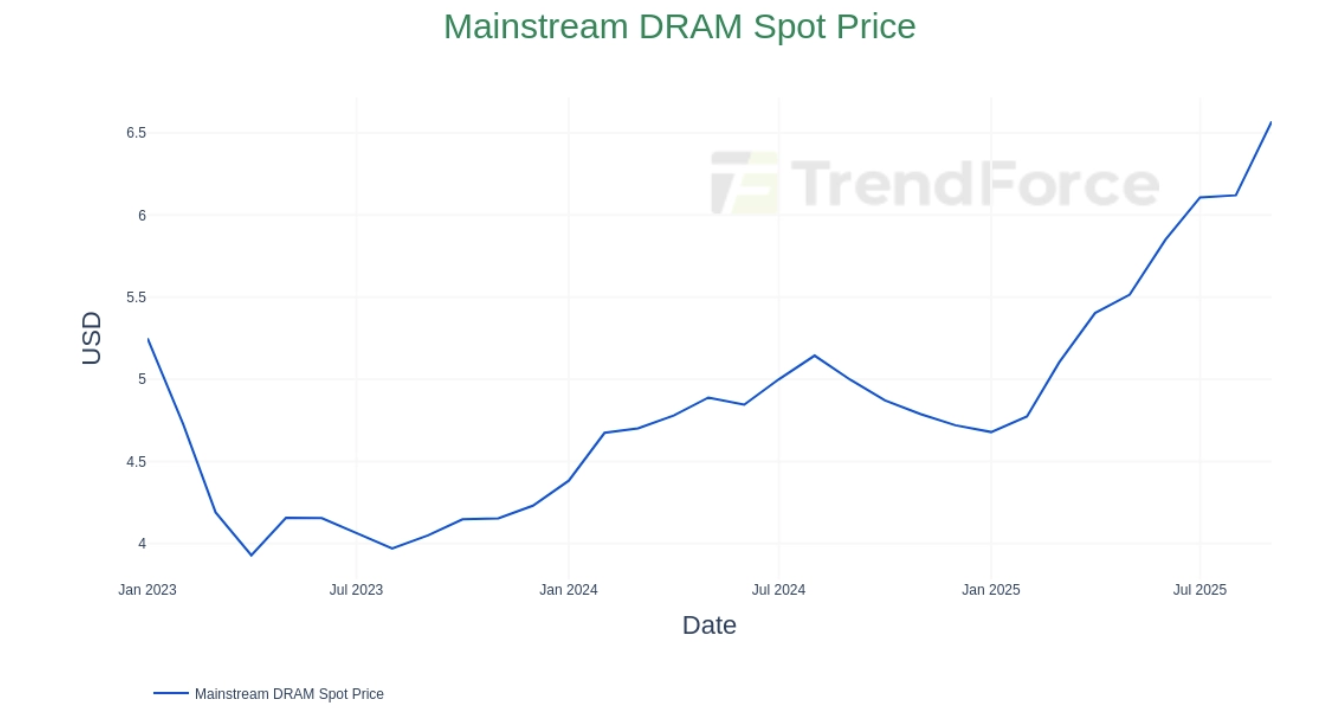

TrendForce’s figures refer to contract pricing. Spot-market indicators can help illustrate near-term sentiment heading into negotiations, but spot pricing does not equal contract outcomes.

Spot pricing momentum can foreshadow negotiation tone, even though contract pricing is set differently.

Spot pricing momentum can foreshadow negotiation tone, even though contract pricing is set differently.

NAND and Enterprise SSD: Elasticity Under Pressure

NAND is often viewed as more elastic than DRAM because density migration provides options. But TrendForce’s upgraded view, combined with public commentary from major suppliers, suggests that “flexibility” is being absorbed by data-center and AI demand.

Public reporting cites a Kioxia executive stating the company’s 2026 NAND production is effectively sold out, with tightness expected into 2027 signaling enterprise pull is crowding out discretionary availability.

For industrial and embedded storage designs, substitutions aren’t always seamless. Flash changes can trigger:

- firmware/FTL validation

- endurance + thermal re-qualification

- system-level re-validation (especially in regulated or long-life environments)

The Hidden Risk: PCNs, EOLs, and Forced Flash Transitions

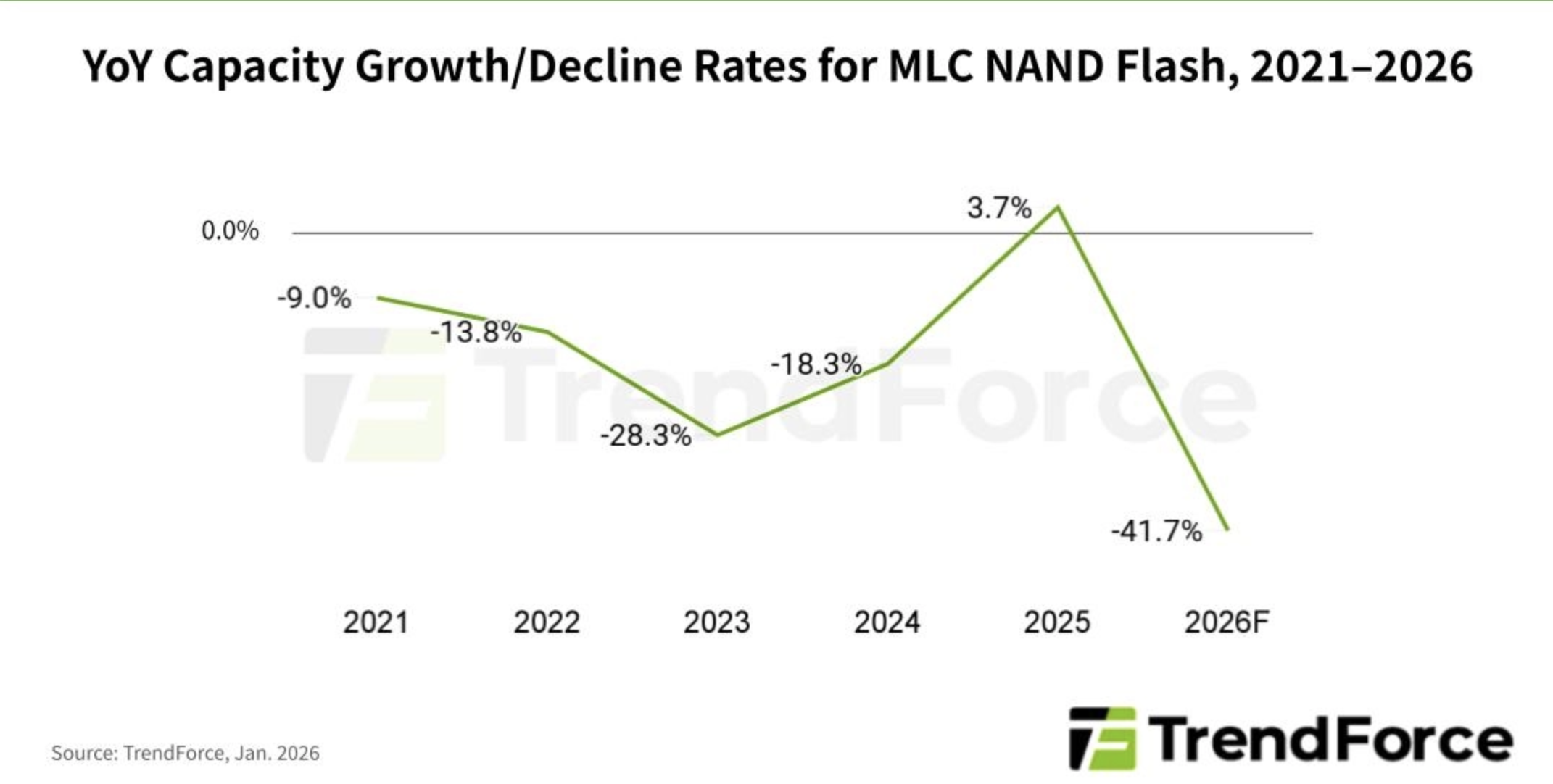

Beyond cyclical pricing, there’s a structural issue in legacy flash: MLC NAND is shrinking into a niche market.

TrendForce reports that the decline in MLC supply is being driven largely by Samsung’s MLC NAND end-of-life plan, with final shipments expected in June 2026, while other major suppliers limit MLC output primarily to existing customer commitments.

For long-life applications still tied to MLC (industrial/medical embedded storage, rugged compute, certain aerospace-grade designs), replacement paths may not be straightforward. Programs may be pushed toward TLC/QLC-based alternatives or redesigns, turning what used to be a roadmap decision into a schedule-risk event.

TrendForce projects a sharp contraction in MLC NAND capacity in 2026, increasing supply risk for long-life applications that still depend on MLC.

TrendForce projects a sharp contraction in MLC NAND capacity in 2026, increasing supply risk for long-life applications that still depend on MLC.

TrendForce’s February revision is a strong warning that 1Q26 is shaping up as an allocation-led market, and supplier commentary increasingly aligns with the view that AI-led demand pressure can persist through 2026 and beyond. In allocation-led markets, the fastest advantage comes from visibility: which SKUs are at risk, which can be dual-sourced, and which require immediate coverage.

IBS can help map at-risk SKUs, validate alternates, and secure coverage across our authorized + independent channels.