U.S. Lawmakers Push to Close Export-Control on Chipmaking Tools Bound for China

Published: 2.16.2026

Key Takeaways

- A bipartisan group of House lawmakers is urging the administration to implement countrywide export controlson critical semiconductor manufacturing equipment, related subcomponents, and servicing destined for China.

- The letter argues that entity-specific restrictions leave enforcement gaps, particularly once equipment enters China and verification becomes limited.

- The push reflects a broader U.S. strategy: limiting not only China’s access to advanced chips, but also its ability to manufacture and sustain advanced semiconductor capacity.

For the past several years, the public debate around U.S.–China semiconductor controls has focused on what chips can be shipped, especially high-end AI accelerators and the performance thresholds that govern exports. But lawmakers are now pushing attention upstream, toward something more foundational: machinery and support ecosystem that makes advanced chips possible in the first place.

A bipartisan group of lawmakers led by John Moolenaar, chair of the House Select Committee on the Chinese Communist Party, and Brian Mast sent a letter to Secretary of State Marco Rubio and Secretary of Commerce Howard Lutnick urging tighter export controls on advanced semiconductor manufacturing equipment (SME) to China.

The letter calls SME controls “one of America’s most significant points of leverage” in strategic competition with China and asks the administration to provide a briefing within a month outlining its plan and timeline to secure allied cooperation on broader restrictions.

The lawmakers argue that the current framework is largely structured around entity-based listings leaving gaps that are difficult to close once equipment crosses the border. They contend that countrywide restrictions on “chokepoint” tools, subcomponents, and servicing would strengthen enforcement and reduce circumvention risk.

Why Lawmakers are Pressing This Now

The letter frames this as a structural issue that existing controls are too narrow can be hard to enforce and easier to work around, especially once equipment is already on the ground.

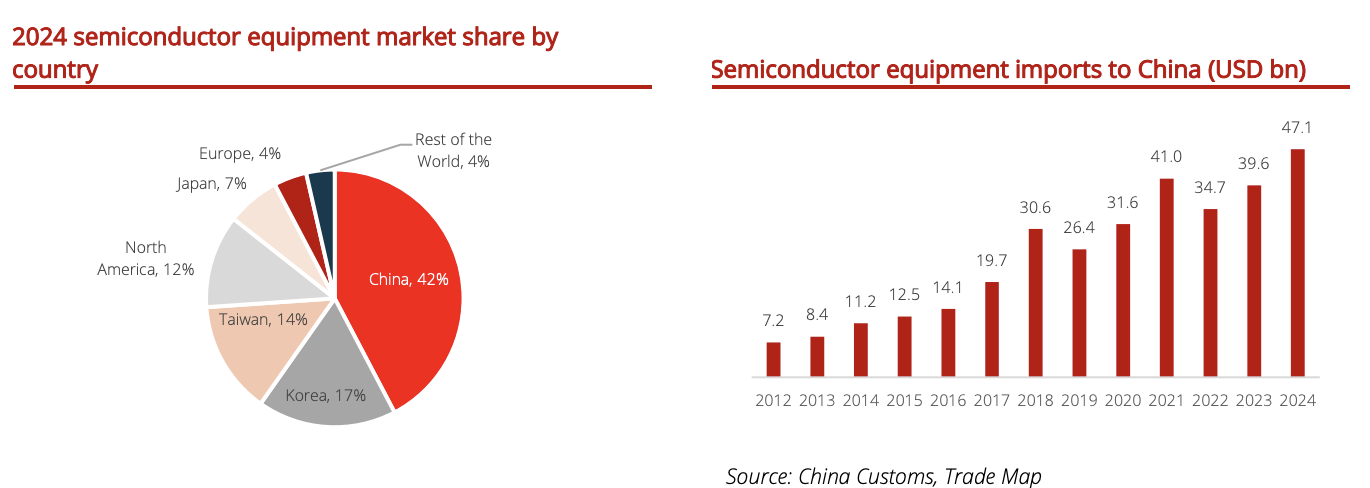

Figure 1. China’s pull on the toolchain remains massive. China accounted for 42% of global semiconductor equipment spending in 2024, while equipment imports remained elevated.

Figure 1. China’s pull on the toolchain remains massive. China accounted for 42% of global semiconductor equipment spending in 2024, while equipment imports remained elevated.

(Source: DBS)

1) Entity-based controls don’t hold up well after shipment

A central claim is that restrictions built around entity lists leave gaps that become extremely difficult to close once equipment crosses the border. Lawmakers highlight practical enforcement constraints: end-use verification can require advance notice and coordination, may take weeks or months to arrange, and can limit the ability to independently confirm compliance after shipment.

Once certain tools enter China, enforcement leverage weakens, so controls that rely heavily on entity-specific listings may not be sufficient for the most sensitive “chokepoint” categories.

2) Chokepoint equipment flows are still a concern

The lawmakers point to continued Chinese demand for foreign chokepoint tools, specifically spotlighting advanced lithography as the “most important chokepoint.” They write that Dutch sales of advanced lithography equipment to China doubled from 2022→2023 and again from 2023→2024, arguing this is evidence that demand remains strong despite evolving rules.

Whether or not every datapoint is debated, the policy thrust is clear: lawmakers believe current restrictions are uneven, and that gaps between U.S. rules and allied rules can create a path around controls.

3) Servicing and upgrades keep tools productive even when new shipments slow

Advanced equipment depends on maintenance, calibration, spare parts, software updates, and field engineering to keep uptime high and output stable. Lawmakers warn that even if exports tighten, installed tools can remain productive as long as they are supported and they encourage restrictions on servicing “to the extent feasible,” framing servicing as a policy lever that can determine whether older tools stay strategically useful.

From Chips to Tools: A Shift Upstream

Since 2022, U.S. semiconductor export controls have targeted both outputs (advanced chips and computing capability), and means of production (the tools and know-how used to fabricate advanced chips).

BIS rules already restrict certain categories of equipment for advanced logic and memory production, along with limits on U.S. persons supporting advanced-node fabrication in China. The lawmakers’ letter argues that these measures should now be expanded in scope and, critically, aligned across allies so restrictions don’t simply shift to the weakest jurisdiction.

A central claim in the letter is that entity-specific controls do not fully mitigate risk once equipment is delivered inside China.

Lawmakers cite practical enforcement constraints, noting that end-use verification visits require advance notice and coordination with Chinese authorities. They argue that such procedures can limit the ability of U.S. officials to independently confirm compliance after shipment.

The letter frames this as a structural challenge rather than a one-off compliance issue, asserting that enforcement complexity increases when restrictions are narrowly applied rather than countrywide.

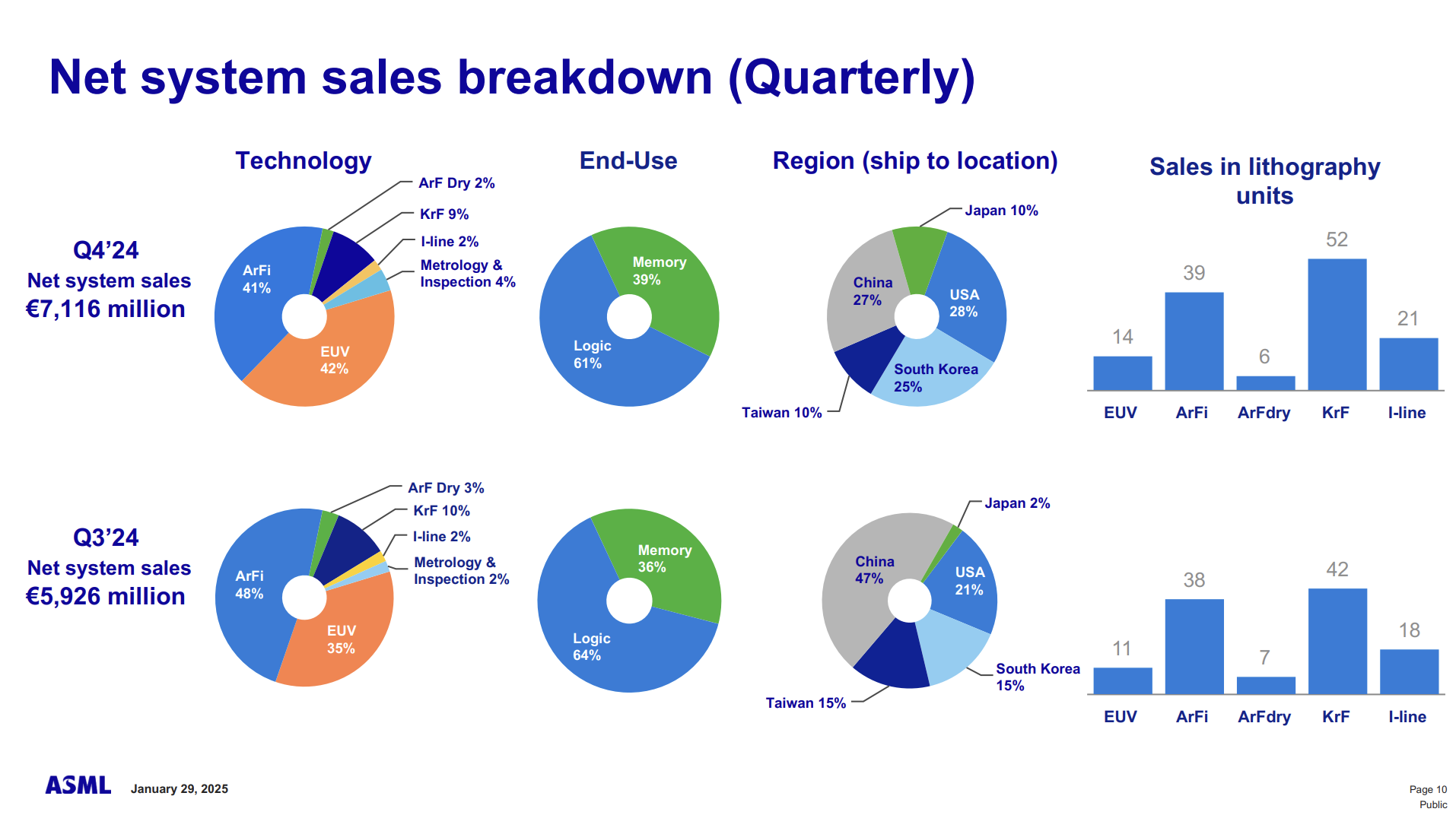

Lithography and Chokepoint Equipment

The lawmakers highlight advanced lithography equipment as a critical “chokepoint” in semiconductor manufacturing. Advanced extreme ultraviolet (EUV) lithography systems are produced exclusively by ASML, and deep ultraviolet (DUV) systems are also central to advanced-node fabrication.

Figure 2. ASML system sales by destination and technology mix (2024 vs 2023). The chart highlights the regional “ship-to” breakdown alongside lithography technology mix.

Figure 2. ASML system sales by destination and technology mix (2024 vs 2023). The chart highlights the regional “ship-to” breakdown alongside lithography technology mix.

(Source: ASML Investor Presentation, FY2024.)

Public financial disclosures from ASML have shown a significant rise in sales to China in recent years. According to the company’s reported results, China accounted for a substantially higher share of total system sales in 2023 and 2024 compared with 2022. Lawmakers cite these increases as evidence that demand for advanced equipment remains strong despite evolving export controls.

The letter argues that without aligned, countrywide controls among the United States and its allies, including the Netherlands and Japan, restrictions may remain uneven.

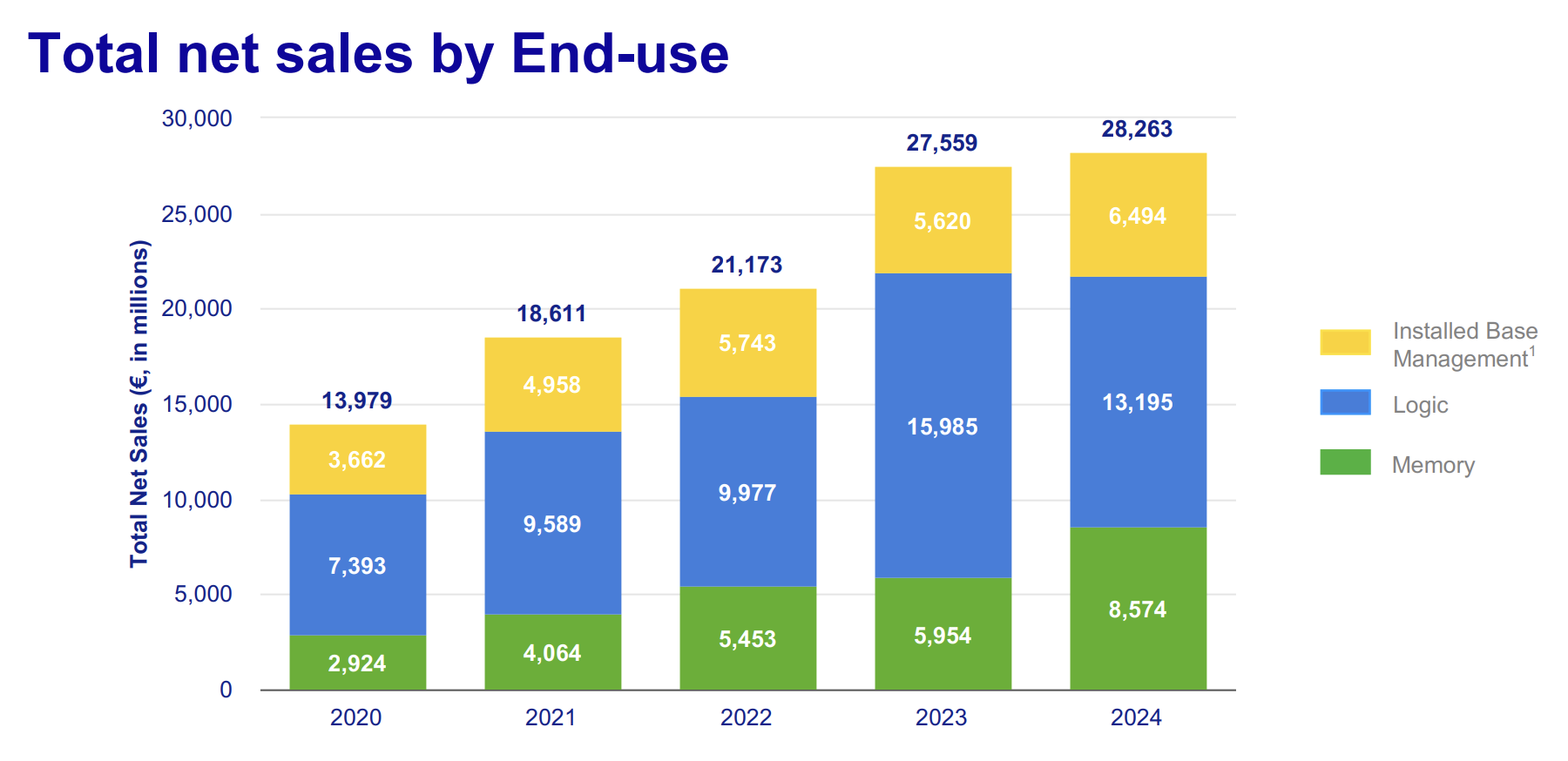

Subcomponents and Servicing as Policy Levers

Beyond primary tools, the lawmakers emphasize subcomponents and servicing as areas requiring attention. They note that advanced semiconductor manufacturing equipment depends on highly specialized parts and technical support, including calibration, software updates, and field engineering services. The letter encourages restrictions on servicing “to the extent feasible,” asserting that installed equipment can remain operational and productive as long as it receives continued support. Subcomponents are also cited as a potential vulnerability. The lawmakers argue that access to critical parts used in tool construction could enable domestic replication efforts over time.

Figure 3. Servicing is a growing business line. ASML’s Installed Base Management has risen alongside overall sales, illustrating why lawmakers are targeting servicing/parts as an enforcement lever once tools are already installed.

Figure 3. Servicing is a growing business line. ASML’s Installed Base Management has risen alongside overall sales, illustrating why lawmakers are targeting servicing/parts as an enforcement lever once tools are already installed.

(Source: ASML Investor Presentation, FY2024.)

What They Want to Prevent: Capability Buildout, Not Just Transactions

The letter is best read as a bid to prevent two long-term outcomes:

A resilient domestic toolchain that erodes leverage

Lawmakers warn that each advanced tool that enters China can reduce future leverage if China develops domestic alternatives and reliance on foreign ecosystems declines. The fear is not just incremental progress but a future where controls become less effective because the toolchain is increasingly localized.

A policy “whack-a-mole” cycle of workaround routes

If restrictions remain uneven across jurisdictions, procurement can shift to wherever rules are less strict; if controls focus only on new shipments, output can be sustained through servicing; if controls are entity-only, enforcement becomes harder after delivery. The letter is essentially pushing for controls that are broader, simpler to administer, and harder to route around.

Slowing Capability, Not Just Transactions

The concerns outlined in the letter align with broader U.S. policy objectives articulated in export-control rulemakings since 2022. The U.S. government has stated that restrictions are intended to limit China’s ability to produce advanced semiconductors that could support military modernization, artificial intelligence applications, and advanced weapons systems.

Congressional analyses have similarly described U.S. export controls as targeting both immediate access to advanced chips and the long-term capacity to manufacture them.

The lawmakers’ warning is framed in forward-looking terms: they argue that each advanced tool that enters China potentially reduces future leverage if domestic alternatives are developed or foreign dependency declines.